Managing operational overhead is a critical priority for farm owners and rural property investors across Northeast Ohio. The Current Agricultural Use Value program offers a powerful statutory mechanism to lower carrying costs on working farmland. Administered under strict Ohio Revised Code guidelines, the Stark County Auditor values qualified land based solely on agricultural productivity and soil classification rather than speculative market values. This definitive guide delivers a comprehensive roadmap to help local owners navigate enrollment criteria, track annual deadlines, and secure maximum legal tax savings across Canton, Massillon, and Alliance.

What is the CAUV Program & The Role of the County Auditor?

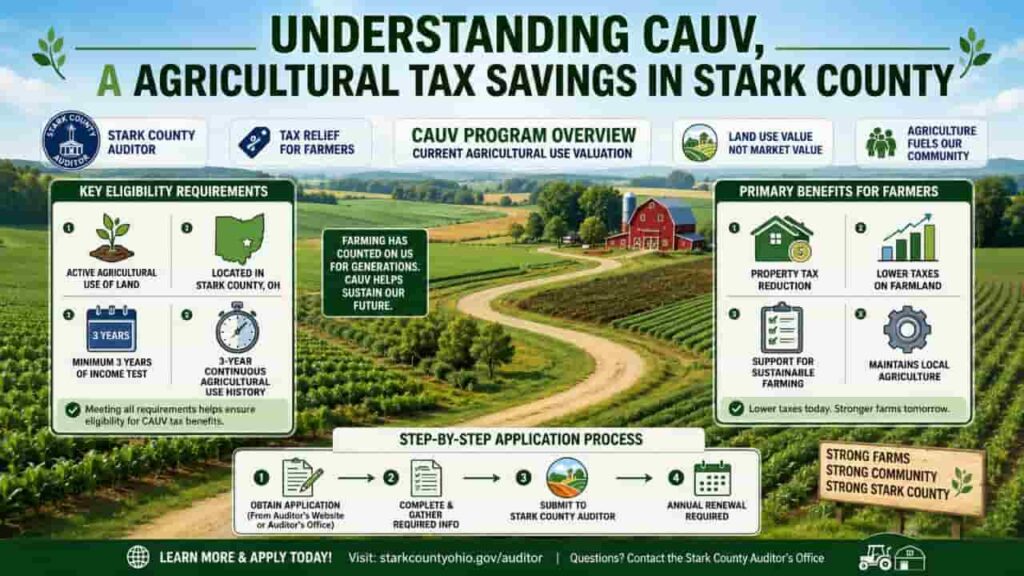

The Current Agricultural Use Value (CAUV) program is a specialized differential tax assessment structure established by the Ohio Legislature in 1974 via a constitutional amendment. It provides substantial, targeted property tax relief to owners who devote their real estate assets exclusively to commercial agricultural production.

Under standard Ohio tax laws, real estate is appraised based on its “highest and best use” baseline meaning a tract of flat farmland near Canton or Massillon could be taxed as if it were a high-value residential housing development or a commercial shopping plaza. The CAUV program legally overrides this market-driven metric, mandating that qualifying land be valued strictly on its current agricultural capacity and capitalized net income potential.

+————————————————————————-+

| Standard Market Valuation Method |

| Taxed on speculative real estate value / residential development potential |

+————————————————————————-+

vs.

+————————————————————————-+

| CAUV Valuation Method |

| Taxed strictly on soil productivity, crop indexes, and farming income |

+————————————————————————-+

The Statutory Role of the Stark County Auditor in CAUV Administration

In Ohio public record informatics, the Stark County Auditor functions as the chief assessment officer and single regulatory gateway for the CAUV system. The Auditor’s office does not merely accept applications; it actively manages the compliance ecosystem through several core administrative roles:

- Mass Appraisal & Formula Enforcement:

The Auditor applies the official capitalization formulas provided by the Ohio Department of Taxation. This involves mapping 100+ distinct soil types across Stark County and matching them against moving 5-year averages for crop prices, non-land production costs, and statutory interest rates. - Application Verification & Field Audits:

The Auditor’s Real Estate Division is legally tasked with reviewing all initial Form DTE 109A submissions. To prevent tax fraud and maintain the integrity of the tax duplicate, the Auditor coordinates periodic on-site field inspections and aerial GIS spot-checks to verify that the acreage is in active, commercial agricultural use. - Recoupment Tracking & Financial Management:

When a property is sold for development or fails to meet compliance standards, the Auditor calculates the mandatory three-year tax savings clawback (recoupment). The Auditor formally logs this penalty as a primary tax lien against the parcel before any new deed transfer is approved. - Annual Renewal Governance:

Every January, the Auditor’s office generates and distributes mandatory annual renewal forms to all registered CAUV tract owners, managing the strict verification pipeline that runs through the first Monday in March.

The Core Economics and Benefits of CAUV

The CAUV program operates as a differential tax assessment system designed to protect Ohio’s agricultural infrastructure from being priced out by suburban sprawl. When farmland is valued at standard market rates, speculative development spikes property assessments, creating artificially high tax liabilities for active working farms.

Implementing a qualified CAUV structure on your real estate yields distinct structural advantages:

- Production-Based Valuations: Assessments are calculated using a complex formula from the Ohio Department of Taxation that analyzes crop prices, production costs, and capitalization rates across specific soil groupings, completely separate from local real estate market spikes.

- Targeted Land Relief: The substantial tax reduction applies directly to the agricultural soil acreage itself. Notably, any residential home sites (typically appraised at a baseline of one acre) and commercial farm outbuildings continue to be assessed by the appraiser at standard fair market value.

- Integrated Legal Shielding: When property owners couple CAUV tax status with an official Agricultural District designation via the Auditor’s office, they unlock statutory protections under Ohio law against specific civil nuisance lawsuits regarding common farm odors, dust, or noise.

Statutory Qualification Parameters

Farmland assets do not automatically qualify for differential billing. Under Ohio Revised Code ORC §5713.30, the underlying parcels must have been devoted exclusively to commercial agricultural operations for the three consecutive calendar years immediately prior to submitting an official application.

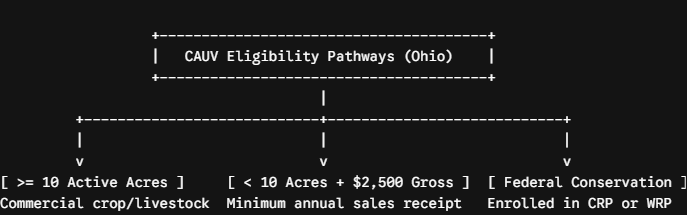

To establish eligibility with the Stark County Auditor’s appraisal division, a farm tract must satisfy at least one of three primary regulatory benchmarks.

The Baseline Acreage Threshold: The property must consist of ten or more contiguous acres utilized exclusively for commercial animal husbandry, aquaculture, timber harvesting, or traditional crop production.

The Small-Farm Income Proving Option: Tracts measuring under ten total acres can still legally qualify if the owner proves the land generates a gross annual income of at least $2,500 directly from the sale of agricultural products.

Federal Conservation Enrollment: Land set aside or completely enrolled in approved federal conservation ecosystems such as the Conservation Reserve Program (CRP) or Wetlands Reserve Program (WRP) automatically maintains qualifying status.

2026 Stark County CAUV Operational Timeline

Filing timelines within the Auditor’s Real Estate Division are governed by strict statutory deadlines. Missing a filing window results in immediate removal from the program and triggers mandatory financial clawbacks.

The table below outlines the updated operational windows, mandatory administrative requirements, and fee profiles.

| Regulatory Phase | Specific Calendar Window | Administrative Requirement |

| Initial Application | First Monday in Jan. to First Monday in March | Requires a $25.00 non-refundable filing fee per farm unit. |

| Annual Renewal | Prior to the First Monday in March | Must be filed annually; there is no fee for timely renewals. |

| Ownership Transfer | Within 60 Days of Deed Recording | New owners must submit a fresh initial application and fee. |

Step by Step Guide: How to Apply for CAUV Tax Status

To seamlessly integrate your agricultural acreage into the county’s specialized tax duplicate without administrative delays, follow this exact procedural workflow.

1. Acquire Official Form DTE 109A: Form Procurement.

Download or print Form DTE 109A (Initial Application for the Valuation of Land at its Current Agricultural Use) directly from the Stark County Auditor’s official web portal or pick it up in person at the county administration building in Canton.

2. Consolidate and Identify All Active Parcels: Asset Mapping.

Locate the precise 7-digit parcel identification numbers via the Auditor’s GIS parcel viewer. Group all continuous or non-contiguous parcels that function together as a single commercial farming unit onto your master application packet.

3. Compile Certified Evidentiary Records: Financial Document Assembly.

For agricultural operations under ten acres, assemble your verifiable financial paper trail. You must attach copies of your federal tax return Schedule F (Profit or Loss From Farming), detailed commercial grain elevator receipts, or point-of-sale livestock invoices validating the $2,500 gross income threshold.

4. Remit Application Packets and Await Field Audit: Submission and Compliance.

Submit the complete DTE 109A packet along with the $25.00 statutory fee to the Auditor’s office before the first Monday in March deadline. Once logged, the Auditor’s appraisal division will schedule an on-site field inspection to visually verify active agricultural production.

The Critical Risk: Recoupment Financial Penalties

While the CAUV framework delivers substantial overhead relief, it functions as a binding conservation commitment to the state. Converting the land use out of active agriculture or failing to return the annual renewal paperwork triggers an automatic Recoupment Penalty.

The Three-Year Clawback Rule: Under Ohio law, if CAUV land is formally removed from the registry or converted to non-agricultural uses (such as commercial building or residential zoning), the Auditor applies an immediate recoupment charge. This penalty equals the exact total tax savings realized by the property owner over the previous three tax years.

These clawback balances attach directly to the land as a primary tax lien, which must be settled before any future real estate transfers can be legally completed.

Expert Strategies for Rural Land Investors

Proactively Manage Parcel Transfers

When buying rural acreage in Stark County that is already listed under CAUV status, do not assume the tax break transfers automatically to your entity. The change in ownership legally voids the prior registration. You must file a new initial DTE 109A application under your own name or LLC within the statutory window, or face an unexpected three-year recoupment bill at closing.

Audit the Soil Survey Matrix via GIS

The primary drivers of your final tax liability are the specific soil type classifications mapped across your property boundaries by the Ohio Department of Taxation. Launch the Stark County Auditor’s interactive GIS Viewer and overlay the soil survey data layers. Understanding how much of your land is classified as prime agricultural soil versus non-productive woodland or steep typography lets you accurately forecast annual tax shifts.

Conclusion

Managing property assessments through the Stark County CAUV program is an indispensable strategy for maintaining a profitable agricultural asset. By utilizing production value instead of speculative market development rates, landowners can significantly lower their annual tax duplicate obligations. Navigating the regulatory landscape requires careful adherence to the timelines enforced by the Stark County Auditor, strict verification of soil type indexes, and regular updates to farm documentation. Implementing these steps effectively secures your land’s financial viability while keeping your operation competitive in Ohio’s evolving commercial market.

FAQs

What is the current CAUV income requirement for small farms?

For properties measuring under ten total acres, owners must present certified financial documentation showing a gross annual income of at least $2,500 from commercial agricultural sales to maintain active eligibility.

What is the deadline for CAUV renewal in Stark County, Ohio?

Property owners must submit their completed annual renewal applications to the Stark County Auditor’s office between the first Monday in January and the first Monday in March of each calendar year.

Does commercial timber production qualify for the CAUV program?

Yes. Land exclusively devoted to timber harvesting qualifies for CAUV status, provided the acreage satisfies the ten-acre baseline and operates under a certified, professional forest management plan.

Can a farm sit fallow for a season without losing CAUV status?

Farmland can occasionally remain completely idle or fallow for up to one year due to standard crop rotation schedules or unexpected illness, without triggering removal or recoupment penalties.

Where can I check my property’s specific soil classifications?

You can view your farm’s exact agricultural soil types and localized capability indexes directly through the Stark County Auditor’s GIS Portal or by contacting the Real Estate Division.