Understanding how tax rates are created and adjusted on the Stark County property search portal is vital for local real estate owners. The structural distinction between Inside Millage and Outside Millage serves as the most critical factor shaping your annual tax liabilities in Ohio. While unvoted inside millage remains constitutionally capped and fixed, outside millage relies entirely on voter-approved ballot initiatives protected by state inflation shields under House Bill 920. This expert guide details the legal mechanics, calculations, and administrative roles governing these property tax structures.

The Administrative Authority of the Stark County Auditor

Before looking at the structural math, it is essential to establish the administrative role of the Stark County Auditor in managing local millage structures. Under the Ohio Revised Code, the Auditor serves as the chief fiscal officer and assessor for all county local government units, townships, municipalities, and public school districts.

The Auditor’s office does not create or vote on property tax rates. Instead, the Auditor acts as a central administrative clearinghouse:

- Rate Certification: The Auditor maintains the official tax duplicate and calculates the 35% taxable assessed value for every property parcel.

- Levy Implementation: Upon receiving official ballot results from the Board of Elections, the Auditor calculates and applies the exact inside and outside millage adjustments required for local budgets.

- State-Level Compliance: The Auditor coordinates with the Ohio Department of Taxation to verify that all applied millage remains compliant with statutory limitations and rate adjustments.

Inside Millage: The Unvoted Constitutional Baseline

Inside Millage represents the bedrock foundation of Ohio’s property tax framework. It is structurally defined as property tax millage that is legally levied without a vote of the public.

The 10-Mill Constitutional Ceiling

Under Article XII, Section 2 of the Ohio Constitution, the state enforces a strict statutory limit on unvoted property taxation: the total amount of inside millage that can be levied against any single real estate parcel cannot exceed 10 mills.

These 10 mills are automatically divided among the various local political subdivisions serving your property—such as the county government, your township or city municipality, and your local public school district.

[Ohio’s 10-Mill Inside Millage Allocation Example]

├── Stark County Local Government ──────► ~2.00 Mills (Unvoted Baseline)

├── City / Township Municipality ──────► ~3.00 Mills (Unvoted Baseline)

└── Public School District ─────────────► ~5.00 Mills (Unvoted Baseline)

=======================================================================

Total Combined Inside Footprint ────────► Maximum 10.00 Mills (Statutory Cap)

Because inside millage does not require voter approval, local government units rely heavily on these fixed funds to handle core operational costs, payroll, emergency services, and basic infrastructure upkeep.

Outside Millage: The Voter-Approved Funding Layer

Outside Millage encompasses all property tax rates that fall outside the 10-mill constitutional limit. Unlike inside millage, these rates cannot be enacted unilaterally by local governments. Every single mill of outside millage must be formally placed on a public election ballot and approved by a majority vote of local citizens.

Outside millage forms the primary funding pipeline for localized community enhancements, public health systems, fire districts, and comprehensive school budgets. These ballot items are typically presented as permanent improvement levies, operational levies, or emergency funding bonds.

Inside vs. Outside Millage: Core Structural Differences

| Functional Parameter | Inside Millage (Constitutional Track) | Outside Millage (Ballot Voted Track) |

| Voter Approval Rule | No Vote Required; constitutionally granted directly to local subdivisions. | Mandatory Vote Required; must win a majority at the public ballot box. |

| Statutory Rate Cap | Strictly capped at a maximum of 10.00 mills per taxing district. | No Cap; limited only by what local voters choose to approve. |

| House Bill 920 Protection | Exempt; rates do not decrease when local property values rise. | Fully Protected; effective rates adjust downward to stop inflationary revenue spikes. |

The Inflation Shield: How House Bill 920 Reshapes Outside Millage

To understand how outside millage appears on your tax statement, you must master the relationship between Gross Millage and Effective Millage. This mechanism is controlled by a vital 1976 Ohio law known as House Bill 920 (HB 920).

When a school district or township passes an outside levy designed to generate a specific dollar amount (e.g., $2 million annually), HB 920 ensures that this collected amount remains completely flat over time. As property values grow across Stark County due to reappraisals or triennial market updates, the gross millage rate voted on the ballot is automatically scaled back to a lower effective millage rate.

[The Economic Impact of House Bill 920]

County Real Estate Market Appreciates / Grows UP ↑

──────────────────────────────────────────────────

Gross Voted Outside Millage Scales Automatically DOWN ↓

──────────────────────────────────────────────────

Result: Tax Revenue Base Stays Stably Flat for Local Schools

Because inside millage is completely exempt from HB 920 reductions, your inside mills will always match their gross face value. However, your outside mills will continuously fluctuate downward as market inflation drives property valuations upward, decoupling your tax bill from scaling directly with property inflation.

Step-by-Step Instructions: Calculating Combined Millage Impact

To clarify how these dual structures apply to your property, follow this step-by-step mathematical roadmap to calculate your annual tax base.

Step 1: Establish the 35% Assessed Value

In Ohio, property taxes are never calculated using 100% of your home’s fair market worth. The state mandates that taxes apply exclusively to your Assessed Value, which is exactly 35% of the appraised market value set by the Stark County Auditor.

$$\text{Appraised Market Value} \times 0.35 = \text{Taxable Assessed Value}$$

- Example: For a Stark County home valued at $250,000:

$250,000 x 0.35 = $87,500

Step 2: Sum the Inside and Effective Outside Rates

Locate your property’s specific tax district code profile on the Auditor’s site. Identify the fixed inside millage (always 10.00 mills or less) and add the current effective outside millage for that specific district.

- Inside Mills: 10.00 Mills

- Effective Outside Mills: 48.50 Mills

- Total Effective Taxing Rate: 58.50 Mills

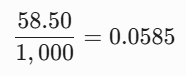

Step 3: Run the Conversion and Multiplication Math

To utilize the millage rate within a baseline currency calculation, convert the total effective mills into a standard decimal format by dividing the rate by 1,000.

58.50 divided by1,000 = 0.0585

Multiply your 35% taxable assessed value by this decimal to find your annual gross property tax obligation before any personalized state rollbacks or homestead exemptions are applied:

$87,500 x 0.0585 = $5,118.75

Local Public Ledger Verification Channels

Property owners looking to review the exact breakdown of unvoted inside mills versus voted effective outside levies for their home can view public records through the following centralized resources:

- Office Name: Stark County Auditor’s Office (Real Estate and Assessment Division)

- Physical Address: 110 Central Plaza South, Suite 220, Canton, OH 44702

- Interactive Digital Search: Access the official Stark County property search application online. Input your unique parcel ID number and open the “Tax Rate” or “Levy Distribution” records tabs to view a complete line-item breakdown of your local rates.

Conclusion

Distinguishing between Inside Millage and Outside Millage is the key to mastering your property tax bills across Stark County. Your property’s annual tax footprint is built on a structured combination of the unvoted 10-mill constitutional baseline and the voter-approved outside levies that fund your local community’s schools and emergency services. By understanding how House Bill 920 continuously modifies effective outside rates while leaving inside millage fixed, you can confidently review your property statements, evaluate local ballot initiatives, and protect your real estate investments.

FAQs

Can inside millage ever exceed 10 mills in Stark County, Ohio?

No. Article XII, Section 2 of the Ohio Constitution enforces a strict, unvoted ceiling cap of exactly 10 mills per taxing district.

Does House Bill 920 lower both inside and outside millage rates?

No. House Bill 920 applies exclusively to voter-approved outside millage. Inside millage is exempt from these adjustments and remains fixed regardless of changing property values.

What is the difference between gross millage and effective millage?

Gross millage is the original tax rate approved on an election ballot. Effective millage is the actual rate applied to your tax bill after being adjusted downward by state law to counter inflation.

Where can I find the exact inside and outside millage breakdown for my Canton home?

You can view these details on the official Stark County property search portal. Look up your individual parcel record and navigate to the “Tax Distribution” tab.

Why do my neighbors across the street pay a different property tax rate?

Even minor location shifts can cross political subdivision or school district boundaries, changing the voter-approved outside millage levies applied to the property.